Accountability of Agency Performance Government in Preventing Fraud With Commitment Organization as Mediator (Case Study in District Fifty Cities)

DOI:

https://doi.org/10.47453/ecopreneur.v6i1.3123Keywords:

Internal Control System, Apparatus Competence, Organizational Commitment, Performance AccountabilityAbstract

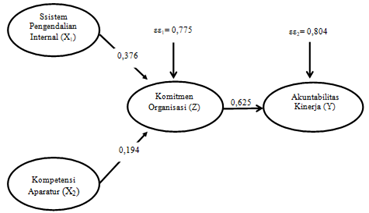

The weak accountability of the performance of government agencies is reflected in the results of the 2021 BPK audit in Fifty Cities Regency which found irregularities in honorarium payments and the use of the budget not in accordance with regional price standards, indicating the weakness of the internal control system and the competence of the apparatus in managing government finances. The purpose of this study was to analyze the accountability of government agency performance in preventing fraud through organizational commitment. The population of the study was the regional apparatus organizations (OPD) in Limapuluh Kota Regency totaling 43 OPDs with sampling using purposive sampling so that the research sample totaled 43 data samples. The data collection technique used a quantitative method approach, namely using a questionnaire filled out by the research sample. Data analysis used path analysis and was processed with the Statistical Package for Social Science (SPSS) version 27. The results of the study found that: (1) the internal control system has an effect on agency performance accountability; (2) the competence of the apparatus has an effect on agency performance accountability; (3) the internal control system has an effect on organizational commitment; (4) the competence of the apparatus has an effect on organizational commitment; (5) organizational commitment has an effect on agency performance accountability; (6) organizational commitment mediates the effect of the internal control system on agency performance accountability; and (7) organizational commitment mediates the effect of apparatus competence on agency performance accountability. The implication of the results of this study is that emphasizing the strengthening of organizational commitment must be the main focus because it is proven to play a significant mediator role between the internal control system and the competence of the apparatus on performance accountability. The recommendation of this study is that the Fifty City Regency Government strengthen its internal control system through periodic audits, transparent reporting, and strict supervision procedures to prevent fraud

Downloads

References

Albrecht , W. Steve and Chad O. Albrecht . ( 2003) . Fraud Examination. Ohio: South-Western.

Armelia, Putu Ayu, and Made Arie Wahyuni. 2020. “Pengaruh Kompetensi Aparatur Desa, Efektivitas Pengendalian Internal, Dan Moral Sesitivity Terhadap Pencegahan Fraud Dalam Pengelolaan Keuangan Desa.” Vokasi: Jurnal Riset Akuntansi 9(2): 61–70.

Atiningsih, S and Ningtyas, AC. (2019). The Influence of Village Fund Management Apparatus Competence, Community Participation, and Internal Control System on Village Fund Management Accountability (Study on Village Government Apparatus in Banyudono District, Boyolali Regency). Journal of Management Science and Applied Accounting. Vol. 10 No. 1 p-ISSN 2086-3748 e-ISSN 2086-3748.

Audit Board of the Republic of Indonesia. (nd). History of the BPK RI. Accessed on April 13, 2024. https://www.bpk.go.id/menu/sejarah .

Dewi, NK, & Gayatri. (2019). Factors that influence accountability in village fund management. E-Journal of Accounting, Udayana University, 26(2), 1269-1298. https://doi.org/10.24843/EJA.2019.v26.i02.p16 .

Ghozali , I. (2018). Multivariate Analysis Application with IBM SPSS 25 Program. Semarang: Diponegoro University Publishing Agency.

Government Regulation 60/2008 concerning the Government Internal Control System.

Hery. (2013). Auditing (Accounting Audit1. Jakarta: CAPS.

Hidayati, Uli, Taris Anggie Fahriza, Early Agista Mahardhika, and Rizdina Azmiyanti. 2022. “Literature Review: Peran Sistem Pengendalian Internal Dalam Pencegahan Kecurangan Akuntansi.” In Seminar Nasional Akuntansi Dan Call for Paper, , 86–95. https://senapan.upnjatim.ac.id/index.php/senapan/article/view/199 (March 2, 2025).

Ichsan, P. (2013). Analysis of Factors Affecting Good Corporate Governance Rating. Semarang: Thesis, Faculty of Economics, Diponegoro University.

IICG, TI (2008). Corporate governance Perception Index. Retrieved 7 9, 17, from www.iicg.orgJannah, SF (2016). The Influence of Good Corporate Governance on Fraud Prevention . Accrual Volume 7 No 2, 177-191.

KabarInvestigasi. (2017). Polsek Wedarijaksa Reveals Case of Embezzlement of Fastabiq Employee Money. Retrieved 7 14, 2018, from https://www.kabarinvestigasi.com/2017/04/polsek-wedarijaksa-ungkap-kasus.html

Karyono. (2013). Forensic Fraud . Yogyakarta.KNKG, KN (2012). Basic Principles and Guidelines for the Implementation of Good Corporate Governance in Banking in Indonesia.

Law of the Republic of Indonesia Number 15 of 2006 concerning the Audit Board.

Law of the Republic of Indonesia Number 17 of 2003 concerning State Finance.

Law of the Republic of Indonesia Number 20 of 2001 concerning Amendments to Law Number 31 of 1999 concerning the Eradication of Criminal Acts of Corruption.

Moeheriono . ( 2014) . Competency Based Performance Measurement Revised Edition,. Jakarta: PT RajaGrafindo Persada.

Perdana, KW (2018). The Influence of Competence of Village Fund Management Apparatus, Commitment of Village Government Organization, Community Participation, and Utilization of Information Technology on Accountability of Village Fund Management in Bantul Regency.

Regulation of the Minister of Home Affairs (Permendagri) Number 113 of 2014 concerning Regional Financial Management.

Santoso, Urip, and Yohanes Joni Pambelum. 2008. “Pengaruh Penerapan Akuntansi Sektor Publik Terhadap Akuntabilitas Kinerja Instansi Pemerintah Dalam Mencegah Fraud.” Jurnal Administrasi Bisnis 4(1). https://journal.unpar.ac.id/index.php/JurnalAdministrasiBisnis/article/view/363/347 (March 2, 2025).

Sedarmayanti. (2017). Human Resource Planning and Development to Improve Competence, Performance and Work Productivity. Bandung: PT Refika Aditama.

Soleman, R. (2013). The Influence of Internal Control and Good Corporate Governance on Fraud Prevention . JAAI Volume 17 No 1, 57-74.

Sugiyono. (2018). Quantitative, Qualitative, and R&D Research Methods, Bandung: Alfabeta.

Widyatama, A and Novita, L. (2017). The Influence of Competence and Internal Control System on Village Government Accountability in Managing Village Fund Allocation (ADD). Indonesian Accounting and Finance Periodical, Vol. 02, No. 02 (2017): 1-20.

Yesinia . et al. ( 2018). Analysis of Factors Affecting Accountability of Village Fund Allocation Management. Journal of Assets (Accounting Research). 10(1): 105-112.

Additional Files

Published

Issue

Section

License

Copyright (c) 2025 Authors

This work is licensed under a Creative Commons Attribution 4.0 International License.